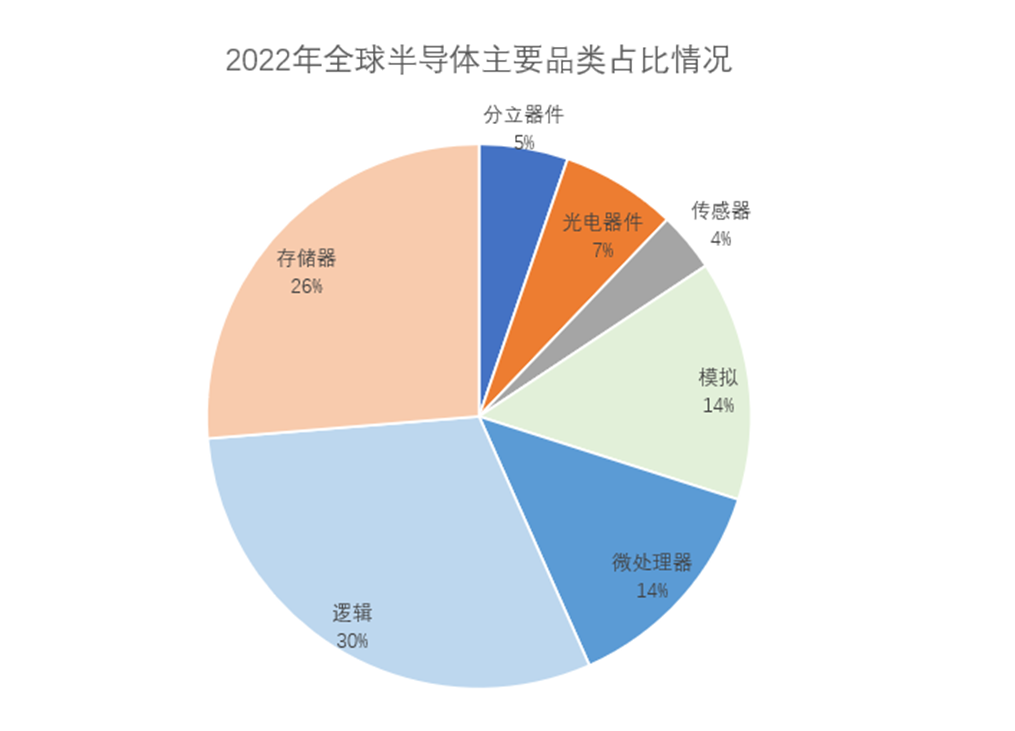

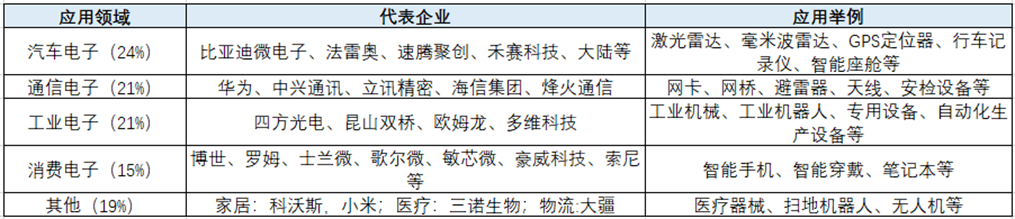

Microprocessor (MPU) can be divided into three categories: computer CPU processor, mobile phone application processor and embedded microprocessor.

Among them, computer CPU processors account for 50% of the MPU market, mainly including PC, server, tablet CPU, and representative companies include Intel, AMD, apple, etc; Mobile application processors account for 30%, and ghostwriting companies mainly include Qualcomm, MediaTek, apple, Huawei Hisilicon, Ziguang Spreadtrum, etc; Embedded microprocessors account for 20%, which are mainly used in smart homes, Internet of things devices and other fields. The representative companies include Quanzhi technology, Ruixin micro, Beijing Junzheng, Jingchen and so on.

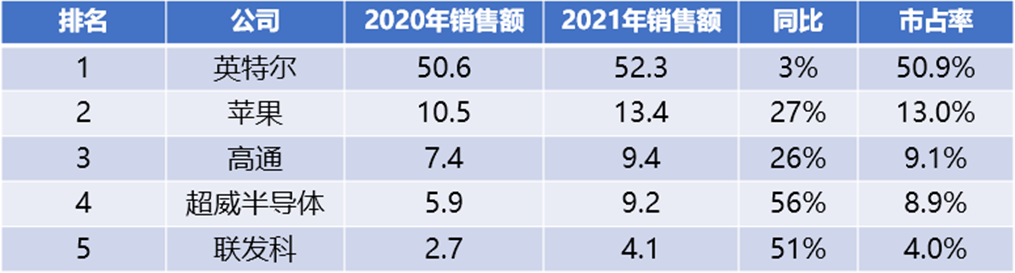

Recently, IC insights, a well-known semiconductor analysis institution, updated the global MPU report. The report shows that the top five MPU suppliers in 2021 are Intel, apple, Qualcomm, AMD and MediaTek, of which Intel is the only one, with a market share of more than 50.9%.

According to the latest data of WSTS, despite the economic difficulties this year, due to the increase of the average selling price (ASP), it is expected that microprocessors will maintain a 5.9% growth in 2022, and the total sales will reach 84.974 billion US dollars.

2. Analog integrated circuits will still maintain a growth rate of more than 20%, and the sales volume is expected to reach 90.338 billion US dollars

Analog chip refers to a chip that processes continuous physical quantities such as light, sound, electricity / magnetism, position / speed / acceleration and natural analog signals such as temperature. It is mainly composed of power management chip and signal chain chip according to product type. Among them, power management chips mainly refer to circuits that manage batteries and electric energy, accounting for about 53% of the analog chip market; The signal chain chip mainly refers to the circuit used to process signals, accounting for about 47% of the market.

Due to the characteristics of analog chip, such as complex product types, long product life cycle, low process requirements, and design process relying on experience, the analog chip market has the characteristics of oligopoly competition. Beyond the Gaohu River, it is difficult for other manufacturers to enter the analog chip industry due to restrictions on technology and talent training; There are many kinds of analog chip products in Hanoi, with low product overlap among different manufacturers and weak competition.

According to IC insights, the world‘s leading analog chip manufacturers are relatively stable, and the top 10 analog chip manufacturers have basically changed little in the past decade. From the data of 2021, the top ten manufacturers account for 70% of the output value of the analog chip industry. Among them, Texas Instruments, adenault and synopsis ranked in the top three with us $14.05 billion, US $9.355 billion and US $5.91 billion respectively. Texas Instruments occupies the leading position in the analog chip industry, accounting for 19% of the global market.

Market share of the world‘s top ten analog chip manufacturers

Source: IC insights; Core starling finishing

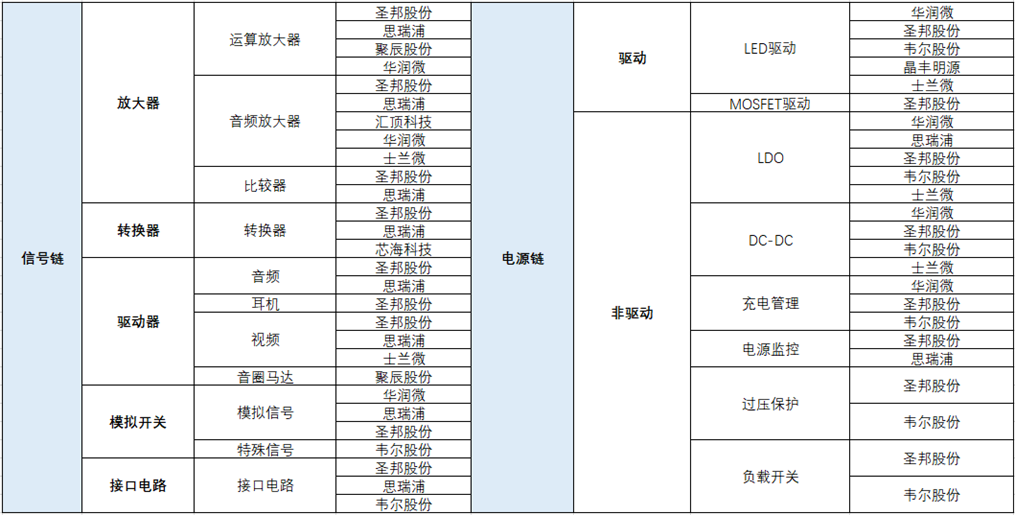

In terms of domestic enterprises, power management chips are widely used and mature, with slow technical iteration and relatively low barriers. Therefore, they are widely distributed in China. Relevant enterprises include Shengbang shares, siliger, Weil shares, Fuman electronics, Zhongying electronics, Quanzhi technology, Jingfeng Mingyuan, sirip, simpeng micro, Shanghai belling, etc; As for the signal chain chip, the domestic layout enterprises mainly include Shengbang, sirip, huiding technology, Xinhai Technology, LanChi technology, Huawei Hisilicon and so on.

Major analog chip manufacturers in China

Source: collated by Starling

As the semiconductor category with the best growth last year, analog chip manufacturers mostly made a lot of money in last year‘s price increase due to lack of core. However, although this year‘s boom continues, there are obvious signs of slowdown in growth. According to WSTS data, it is expected that the global analog chip sales will reach US $90.338 billion in 2022, an increase of 21.9% year-on-year. This figure looks good, but it has dropped by nearly 11 percentage points compared with the 33.1% growth rate last year.

Previously, Ti, the global analog chip leader, informed customers that the imbalance between supply and demand would ease in the second half of the year, making analog chips led by power management chips begin to face downward pressure. In addition, the industry has even heard that the price of some consumer chips of STMicroelectronics has dropped by 80% in the past two months. The dynamics of the above leading manufacturers seem to be releasing a dangerous signal: analog chip manufacturers are also beginning to see product structural differentiation. Everyone can only maintain sustainable profits by dynamically adjusting their product structure and customer structure according to market demand.

2、 Discrete devices are expected to grow by 10.1% year-on-year, with sales reaching 33.408 billion US dollars

Discrete devices refer to electronic devices that have separate functions and cannot be separated. According to the power and current indicators, it is divided into two categories: small signal devices (dissipation power is less than 1W or rated current is less than 1a) and power devices (dissipation power is not less than 1W or rated current is not less than 1a).

Power devices are one of the important basic components in power electronics industry, which are widely used in power conversion and circuit control of power equipment. As the core of electrical equipment and systems, the role of power devices is to achieve the processing, conversion and control of electrical energy. They manage more than 50% of the global electrical energy resources and are widely used in smart grids, new energy vehicles, rail transit, renewable energy development, industrial motors, data centers, household appliances, mobile electronic equipment and other aspects of national economy and national life, It is an indispensable core semiconductor product in the industrial system. Among them, field effect transistor (MOSFET) and insulated gate bipolar transistor (IGBT) are representative.

1. MOSFET will maintain a compound growth rate of 6.7% and is expected to reach US $11.847 billion by 2025

MOSFET, i.e. metal oxide semiconductor field effect transistor. It is called the most ideal power device because of its advantages such as low driving power, fast switching speed, high operating frequency and strong thermal stability.

Compared with other power semiconductor products, MOSFET has the advantages of high switching frequency and strong stability, so MOSFET is mostly used in automobile, industry and other fields. According to MEMS prediction, in the proportion of MOSFET terminal applications in 2022, automobiles will account for 22%, computers and storage will account for 19%, and industry will account for 14%.

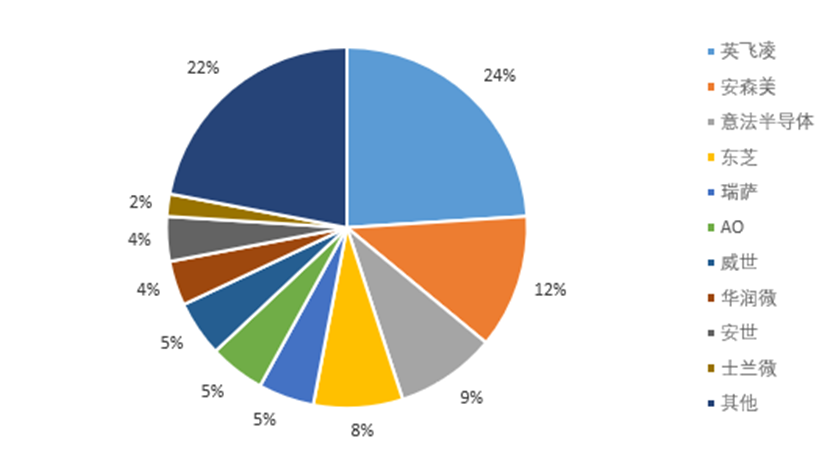

In 2020, the global MOSFET market size reached 8.067 billion US dollars. It is expected that in the next five years, the MOSFET will maintain a growth rate of no less than 6.7% and the market size will reach 11.847 billion US dollars by 2025. In terms of market pattern, Infineon accounted for 24% of the global MOSFET market in 2020, ranking first. China Resources micro, Anson semiconductor and Shilan micro were among the top ten enterprises in the world, with market shares of 3.9%, 3.8% and 2.2% respectively.

Global MOSFET market pattern in 2020

Source: omdia, collated by Starling

Benefiting from the increasingly in-depth wave of domestic substitution in the semiconductor industry, the revenue of domestic MOSFET manufacturers has grown rapidly at present, with China Resources micro, Yangjie technology, China microelectronics, new clean energy, Shilan micro and Dongwei semiconductors as the representatives. It is worth mentioning that CR micro has been deeply involved in MOSFET for many years, and has grown into a MOSFET manufacturer with the largest operating income and the most complete product series in China.

2. IGBT supply exceeds demand, and is expected to increase by 13.96% year-on-year to $8.08 billion in 2022

IGBT is a fully controlled voltage driven power semiconductor device composed of BJT and MOSFET. IGBT has the advantages of high input impedance of MOSFET, fast switching speed, low control power, low BJT on-voltage, large on-state current and low loss. It is widely used in the medium and high voltage field of 650-6500v and is the most promising track in the field of power devices.

According to different manufacturing technologies and downstream application scenarios, IGBT has three types: single tube, IGBT module and intelligent power module IPM. In 2021, the global IGBT market size is about 7.09 billion US dollars, close to 50 billion yuan. It is expected that the global market scale of IGBT will increase by 13.96% to US $8.08 billion in 2022. Among them, the Chinese market accounts for about 40% of the global market.

Global IGBT market scale and forecast

Source: collated by Starling

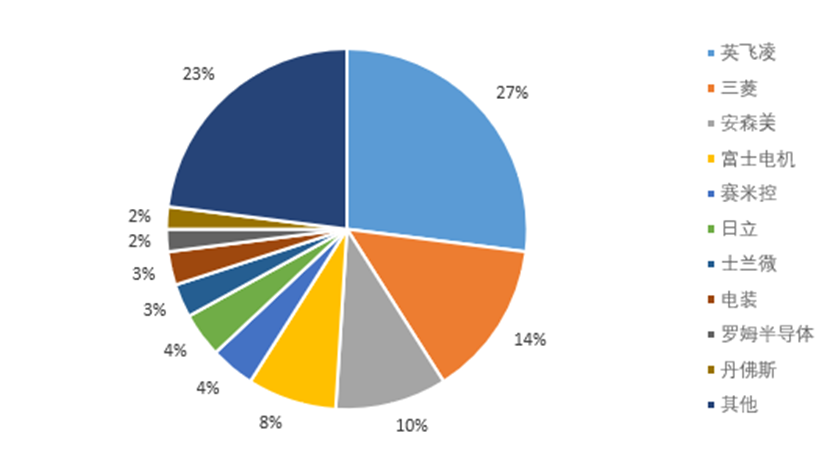

From the perspective of the global IGBT competition pattern, the industry is relatively concentrated. According to yole‘s data, the industry CR3 reached 50% in 2020, and Infineon is the absolute leader of the industry, with a market share of 27%. In addition to Infineon, Mitsubishi Electric, Anson beauty and Fuji Electric currently account for more than 8% of the market; From the domestic perspective, domestic enterprises with perfect IGBT industrial chain layout include BYD semiconductor, star semiconductors, CRRC times electric, and Shilan micro. In addition, many enterprises such as Hongwei technology, Zhixin semiconductor, xinjieneng and Huada semiconductor also have IGBT products or technical reserves, and some of their products have been mass-produced and shipped in new energy vehicles, industrial control and other fields.

Global IGBT competition pattern in 2020

Data source: yole, collated by Starling

According to the latest delivery dates and price trends of Infineon and Anson, the major power semiconductor manufacturers, the delivery dates of IGBT and MOSFET products are generally more than 39 weeks, and the longest can reach 52 weeks. In addition, thanks to the explosion of new demand for new energy vehicles, photovoltaic, energy storage and other products, the prices of the above-mentioned products have been in a stable and rising trend.

The delivery time and price trend of Infineon and Anson IGBT

Data source: Fuchang electronics, compiled by SMIC

According to the data statistics of WSTS, although discrete devices only account for 5.28% of the sales of the semiconductor industry, they are still expected to maintain a growth of 10.1% in 2022.

3、 Sensors differentiated, but still expected to grow by 16.6% to USD 23.184 billion

Transducer / sensor is a kind of detection device, which can feel the measured information and convert the sensed information into electrical signals or other required forms of information output according to certain rules, so as to meet the requirements of information transmission, processing, storage, display, recording and control. It is a bridge connecting the physical world and the digital world.

According to different products, sensors can be divided into MEMS sensors, CIS sensors, RF sensors, radar sensors, fingerprint sensors, etc. MEMS sensors account for the largest proportion, about 29.7%.

1. The downstream demand of MEMS sensors is slowing down, and the price competition is fierce

As the name implies, MEMS sensor is a sensor that uses MEMS technology. Compared with traditional sensors, MEMS sensors have the advantages of small size, light weight, high integration, intelligence, low cost, low power consumption, large-scale production, etc. MEMS sensors are especially widely used in mobile phones, such as magnetic sensors, fingerprint sensors, environmental sensors, etc.

From the perspective of the global market pattern, in the global MEMS sensor market in 2020, Bosch ranked first with a market share of 14.2%, followed by Broadcom and Verizon, with a market share of 9.8% and 5.6% respectively, while ge‘erwei ranked sixth with a market share of 3.9%; In China, goer shares ranked first with a 55% share, followed by Huatian technology and China Resources micro, accounting for 12% and 10% respectively.

Distribution of global MEMS sensor market in 2020

Data source: collated by Starling

2. The supply of lidar sensors is not in demand, and the orders of major manufacturers have soared

From the perspective of downstream applications, automotive electronics is the largest application field of sensors, accounting for 24%. With the gradual popularity of lidar and millimeter wave radar in new energy vehicles in recent years, the application proportion of sensors in the automotive field will continue to increase in the future, and it will be one of the main tracks for the future development of sensors.

Main application fields of sensors

Data source: collated by Starling

In the field of lidar, according to yole‘s data statistics, Valeo, a French first-class automobile supplier, ranks first with 28% of the market share, while Suteng juchuang, a local enterprise, ranks second with 10% of the market share, and luminar ranks third with 7% of the market share. In addition to Sudeng juchuang, Chinese enterprises on the list also include Lanwo Technology (Dajiang), Hesai technology, tudaton, Huawei, etc., with a total of 26% of Chinese enterprises.

Source: yole

In terms of sales data, according to WSTS statistics, the global sensor sales in 2021 will be 19.149 billion yuan, and it is expected to increase by 16.6% year-on-year to 22.319 billion yuan in 2022.

From the market situation, the continuous decline of mobile phone shipments has led to the saturation of the consumer market, and the growth of sensors in the consumer electronics field will tend to be flat in the future. It can also be seen from the semi annual reports of the leading MEMS sensor manufacturers geerwei and Minxin that in the first half of the year, due to the slowdown of downstream demand and fierce price competition, the year-on-year profits began to decline, and Minxin even turned from profit to loss.

In sharp contrast to the consumer market, the automotive sensor market is in short supply. According to Sudeng juchuang, the company has received fixed-point orders from more than 50 models such as BYD, FAW Hongqi, gac-e‘an, jikrypton, Weima automobile and lotus. Driven by strong downstream demand, the company‘s order volume in the first half of this year increased by more than 10 times compared with the same period last year.

4、 The rising momentum of optoelectronic devices is weakening, and the overall price is in a steady downward trend

Optoelectronic devices refer to various functional devices made by using the electric photon conversion effect, as well as accessories or auxiliary articles such as reflectors or mounting hardware supporting such products. This is a diversified product category, including optical fiber transmitters and receivers, LCD, led, OLED, AMOLED and VFD displays, El wires, incandescent lamps, lasers, light tubes, xenon flash tubes and many other product types.

According to different functions, optoelectronic devices can be mainly divided into optical fiber communication devices and optoelectronic lighting devices.

1. Optical fiber communication devices are monopolized by foreign manufacturers, and the domestic proportion is low

Among them, optical fiber communication devices include optical active devices (such as lasers, optical transceiver modules, etc.), and optical passive devices (such as optocoupler, optical fiber switch, optical demultiplexer, etc.).

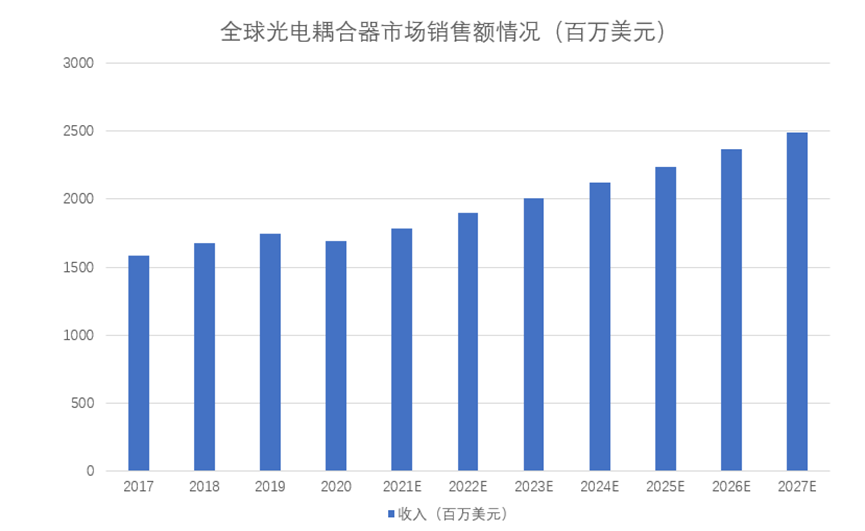

Taking optocoupler as an example, optocoupler (optocoupler for short) is the most commonly used isolation device in high-voltage and low-voltage circuits, and is widely used. In recent years, with the rapid development of new energy vehicles, photovoltaic inverter, servo frequency conversion, smart home appliances, communications, ultra-high voltage power and other industries, the demand for optocouplers has been increasing.

According to the research data of QY research, the global total output value of optical couplers was 1.691 billion US dollars in 2020, and it is expected to maintain a compound annual growth rate of 5.65% in the next seven years. By 2027, the total output value will reach 2.487 billion US dollars. From the perspective of shipment, the global total shipment in 2021 was 38.455 billion, and it is expected to reach 69.222 billion by 2027, with an annual compound growth rate of 10.29%.

Source: QY research; Core starling finishing

In 2021, the first tier manufacturers of optical couplers in the world mainly include Anson, Toshiba and Broadcom, accounting for 44.54% of the market share in total; The second tier manufacturers include Weishi, Risa electronics, sharp and Lite on, with a total share of 25.23%. It is worth mentioning that at present, the main suppliers of the aforementioned optocouplers account for more than 95% of the high-end market, while those in Chinese Mainland account for less than 3%.

2. The demand for photoelectric lighting devices is weak, and the proportion of domestic manufacturers is gradually increasing

Photoelectric lighting devices refer to LCD, led, OLED and other devices that need electricity to light.

Taking OLED as an example, the full name of LED is (organic light emitting diode), that is, organic light emitting diode, which refers to an organic semiconductor composed of an extremely thin organic material coating and a glass substrate and emits light when a current passes through.

As a new generation of display technology, OLED has better display performance than LCD. It has the advantages of good display effect, low power consumption, high flexibility and ultra thin. It is widely used on the screens of smart phones, automotive electronics, intelligent wearable devices, VR devices and other products. OLEDs can be divided into AMOLED and PMOLED according to the driving mode.

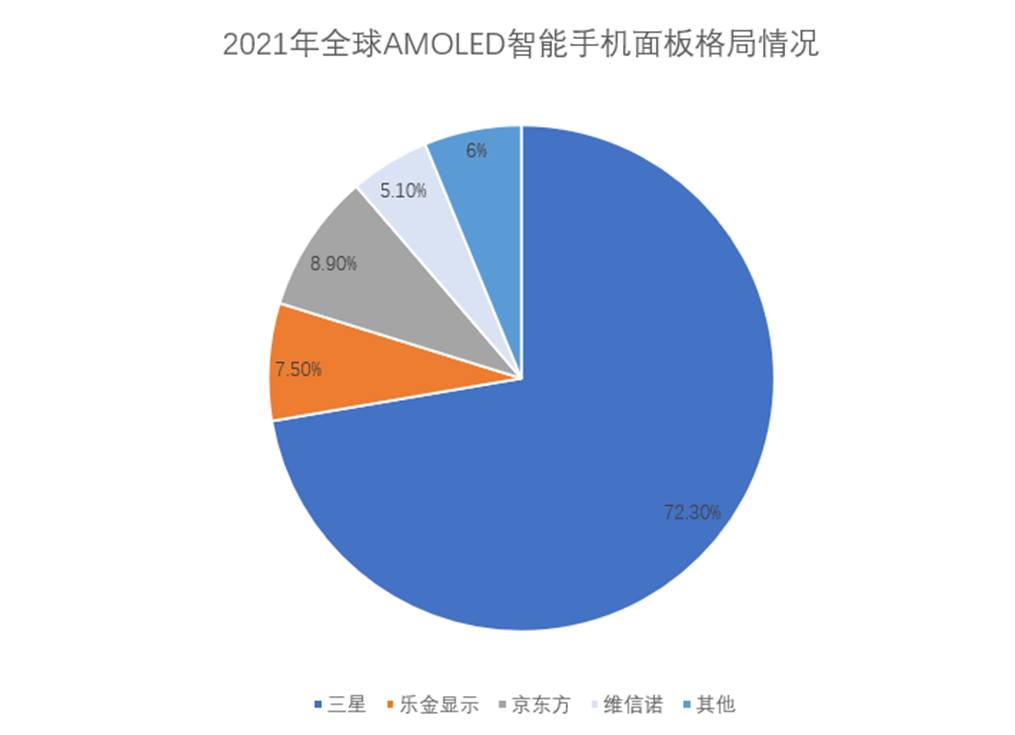

According to cinno research data, in 2021, about 668 million AMOLED smart phone panels were shipped in the global market, an increase of 36.3% year-on-year. Among them, the AMOLED smartphone panel shipment share in South Korea is nearly 80%, and it is still the main force; The domestic manufacturers‘ share of shipments steadily climbed to 20.2%, an increase of 3.7 percentage points year-on-year.

From the perspective of enterprises, Samsung shipped about 480 million AMOLED smart phone panels, with a year-on-year increase of 28.8% and a market share of 72.3%; LG display (LGD) shipped about 50 million AMOLED smart phone panels, with a year-on-year increase of 47.1% and a market share of 7.5%; In China, BOE shipped about 60 million AMOLED smart phone panels, with a year-on-year increase of 67.2% and a market share of 8.9%, with a year-on-year increase of 1.6 percentage points, ranking second in the world and first in China. Visionox‘s AMOLED smartphone panel shipment was about 30 million pieces, with a year-on-year increase of 111.1% and a market share of 5.1%, with a year-on-year increase of 1.8 percentage points, ranking fourth in the world and second in China.

Source: cinno research; Core starling finishing

In 2022, some terminal brands still take inventory adjustment as the priority strategy, and stock up is mainly conservative. The overall demand for smart phone panels is relatively weak, and the supply and demand are still in a loose state. In general, the price of smart phone panels has shown a steady decline.

WSTS expects that the growth momentum of optoelectronic products will be weak in 2022. It is expected that the market scale this year will be roughly the same as that of last year, with a slight increase of 0.2% and an amount of US $45.12 billion.

Write at the end

From the supply side, in addition to vehicle specification products such as MCU, PMIC, IGBT, silicon carbide, MOS and a small number of products such as industrial control power management chips and amplifiers, the supply of most chips has been alleviated, and many consumer grade products such as memory, CIS sensors, display driver chips, LED driver chips, MCU, power management chips, PA and filters have even been oversupplied.

Although the short-term semiconductor industry has entered the inventory adjustment cycle, and is generally expected to last until the first half of 2023. However, in the long run, under the development trend of digitalization and intelligence, the overall demand of the semiconductor market is still relatively strong, and domestic substitution will still be the main theme in the future.

Looking forward to 2023, WSTS will lower its annual growth forecast from 5.1% to 4.6%, but it is expected that all major product categories of semiconductors will still maintain the growth trend, of which higher logic devices and analog devices are still expected to maintain a growth rate of more than 5%.

.

.

Service mailbox

Service mailbox 13823783658

13823783658 ChatNow

ChatNow